Menu

Menu

Menu

Menu

As U.S. banking policies continue to evolve in response to economic conditions, regulatory shifts, and financial crises, new investment opportunities emerge in various sectors. From changes in interest rates to new banking regulations aimed at improving market stability, investors need to stay agile to capitalize on emerging trends. This article explores the impact of recent banking policy changes on the investment landscape, focusing on new opportunities for capital allocation, asset diversification, and portfolio growth.

1. Shifting Interest Rates and Investment FlowsA key aspect of U.S. banking policies is the adjustment of interest rates by the Federal Reserve. As banking regulations evolve, they often lead to changes in monetary policy, which directly affects interest rates. These fluctuations can have a significant impact on the cost of borrowing and the availability of credit.

By understanding how interest rate changes impact the cost of capital, investors can adjust their strategies to benefit from favorable environments and protect against less favorable ones.

2. Impact of Regulatory Changes on Financial InstitutionsU.S. banking regulations play a crucial role in shaping the behavior of financial institutions and, by extension, the broader economy. Changes to regulations can affect banks' lending practices, capital requirements, and the overall stability of the financial system, creating both risks and rewards for investors.

In general, the regulatory framework surrounding U.S. banks shapes the flow of credit in the economy and provides investors with insights into potential sectors that may benefit from changes in lending practices.

3. The Role of Financial Technology (FinTech) in Changing PoliciesThe FinTech sector is one of the most dynamic areas for investment in the current environment. As U.S. banking regulations evolve to address digital banking and online financial services, FinTech companies stand to benefit from the growing demand for innovative financial products.

For investors, FinTech presents an exciting opportunity to tap into the future of banking, where digital transformation and disruptive technologies are shaping new business models and expanding access to financial services.

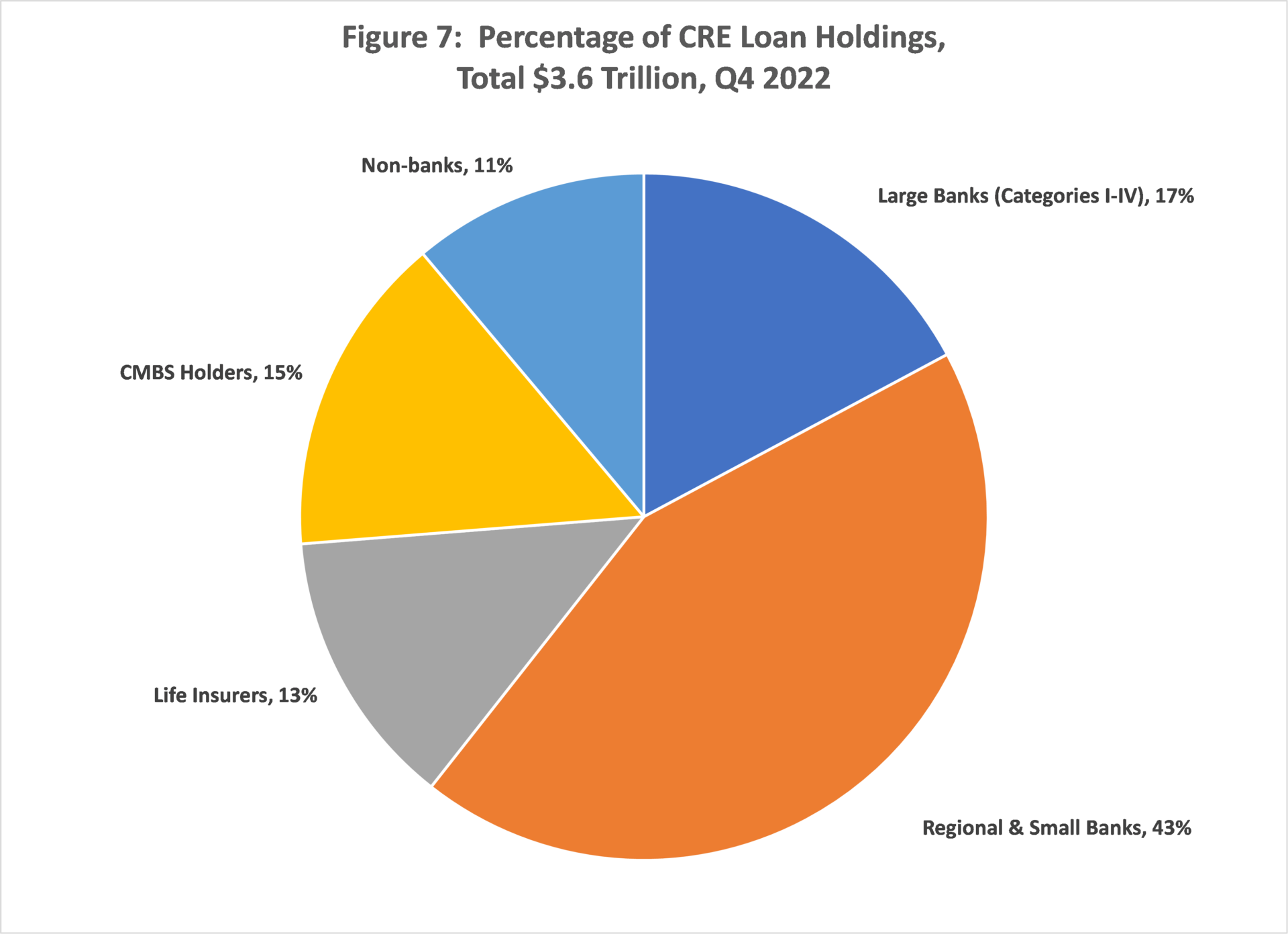

4. Real Estate Market Shifts and Banking RegulationsReal estate investment is another area where U.S. banking policies can have a significant impact. Changes in lending regulations, including mortgage guidelines, influence the availability of housing loans and the cost of homeownership, which in turn affects the real estate market.

Understanding these dynamics allows investors to adjust their strategies based on the current state of the real estate market and the regulatory environment.

5. Risk Management and Investor StrategyAs U.S. banking policies change, the risk landscape for investors evolves as well. Effective risk management becomes increasingly important as investors navigate the uncertainties of shifting regulations.

Swipe. Select. Stay informed.

![]()

![]()

The Federal Reserve has raised interest rates in response to persistent inflation concerns, aiming to stabilize prices and maintain economic stability. The hike is expected to impact borrowing costs, mortgage rates, and financial markets in the coming months

Wells Fargo is launching its new digital wallet, designed to compete with major fintech players like PayPal and Apple Pay. The new wallet aims to provide secure, seamless digital payments, leveraging Wells Fargo’s existing infrastructure and customer base

In response to the COVID-19 pandemic, banks are introducing new remote banking options to ensure customer convenience, safety, and accessibility. These digital transformations are reshaping how customers interact with their financial institutions

The Small Business Administration (SBA) has highlighted its lending programs as key drivers for small business growth. These programs, including the 7(a) loan and 504 loan, provide crucial funding to entrepreneurs, especially those from underrepresented communities.

The Connection Between Banking Rules and Investment Returns

How U.S. Banking Policies Influence Investment Choices

How U.S. Banking Policies Have Evolved Over Time

U.S. Banks' Response to New Investment Regulations